Delta Returns to Solid Profits

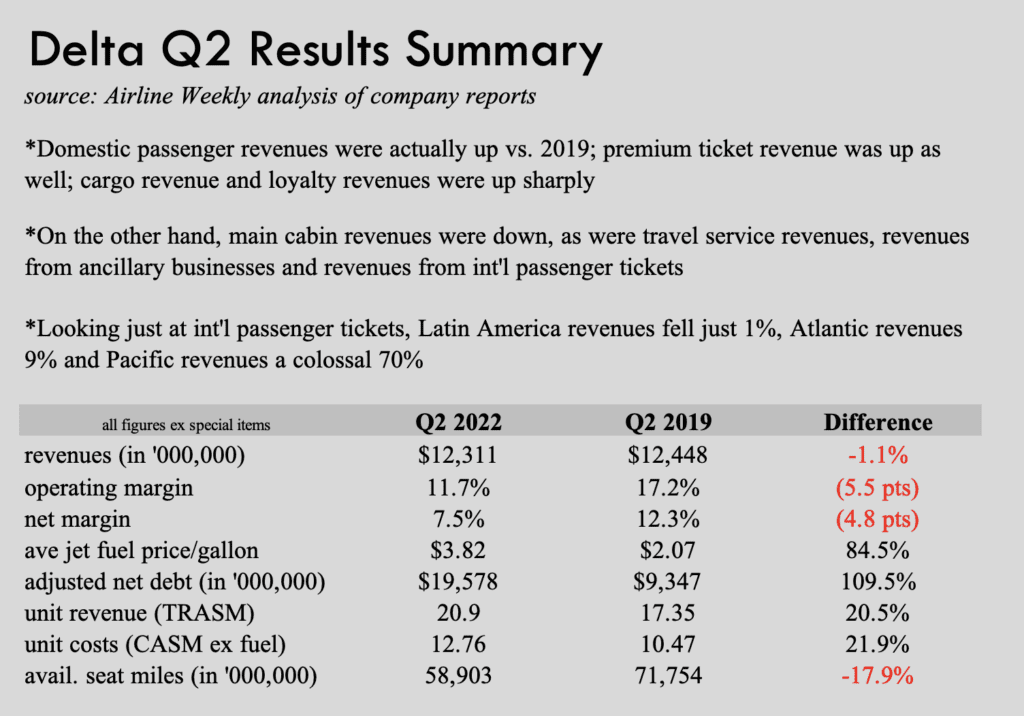

Delta Air Lines opened second quarter airline earnings season on a positive note, unveiling a 12 percent operating margin excluding special items, driven by a strong recovery in domestic passenger demand —especially premium demand. That’s a big step up from the heavy losses Delta and the rest of the airline industry experienced in 2020 and 2021. But that 12 percent figure doesn’t quite represent a total comeback from 2019 — Delta’s second quarter operating margin that year topped 17 percent.

Passenger demand, to be sure, has never been stronger, at least excluding demand to Asia, normally an important market for Delta. The airline is getting a lot more money to fly one passenger one mile today than it was pre-pandemic — total unit revenues (TRASM) rose nearly 21 percent in the second quarter compared to 2019. Unfortunately, the cost of flying one passenger one mile increased more, even excluding fuel; non-fuel unit costs (CASM) rose more like 22 percent. Average fuel prices, meanwhile, were roughly 85 percent higher. Delta’s non-fuel CASM, more encouragingly, will improve as the airline restores capacity, including the widebody flying to Asia its cut sharply. During the June quarter, its total capacity was still down 18 percent versus the same quarter in 2019. Delta plans to hold capacity at the 80-85 percent of 2019 level through the end of the year.

In addition to the high fuel prices, the lagging Asian recovery and the suboptimal asset utilization, Delta wasn’t immune from the operational mayhem plaguing the airline sector as demand suddenly and forcefully revived this spring. But CEO Ed Bastian insisted things have improved thus far in July. Air traffic control staffing shortages are one reason for the many delays and cancellations. Delta also acknowledged difficulties with its own staffing — not so much attracting qualified people (few problems there) but in the time required to train them and have them gain experience. It’s a problem Bastian said temporary but likely to last through the end of the year.

June alone by the way, yielded a 17 percent operating margin for Delta, which augurs well for the peak summer periods of July and August. Indeed, the airline said bookings continue to be strong, even into the seasonally softer autumn period. Premium domestic demand and leisure demand led the recovery, but international and business demand is now building as well.

But what if there’s a recession, as some economists now fear? Bastian made the point that Delta is much better positioned to withstand a downturn than it was in 2009, the last time the economy contracted prior to Covid. Even then, Delta managed to stay profitable excluding fuel hedge losses. Today, the airline’s revenue base is much more diversified, with greater contributions from premium products, loyalty relationships, and cargo and auxiliary businesses like aircraft and engine maintenance.

Delta is excited about the upgraded facilities it has in airports like LaGuardia, Los Angeles, and Salt Lake City. It’s working to regain its investment grade credit rating. SkyTeam membership signups are at record levels. And its operating profit margin in the September quarter should be similar to those in the second quarter, 11-13 percent.

As a reminder, Delta spent much of the 2010s outperforming American Airlines and United Airlines, aided by its Atlanta operation, likely the most profitable airline hub in the world. Its billion-dollar relationship with American Express, mostly non-union workforce, transatlantic joint venture with Air France-KLM and Virgin Atlantic, productive in-house maintenance team, reputation for good service … these are just some of the reasons for Delta’s success since emerging from bankruptcy and merging with Northwest Airlines just before the 2008-09 financial crisis. Its next big move could involve a big narrowbody aircraft order, with reports suggesting interest in the Boeing 737-10 as well as more Airbus A220s.

In Other News

- The Lufthansa Group also sees profits in the June quarter. In a guidance update, it forecast adjusted earnings before interest and taxes (EBIT) of €350-400 million ($353-403 million) in the quarter, driven particularly by the performance of Lufthansa Cargo but also strong demand at its passenger airlines. But, despite that demand, Lufthansa's passenger business — with the exception of Swiss — is forecast to lose money in the quarter. Revenues of roughly €8.5 billion are expected for the period.

- Bankrupt SAS is urging its striking pilots to resume mediation. As of July 14, the industrial action had caused 2,550 flight cancellations affecting more than 270,000 passengers. It was costing 100-130 Swedish krona ($9.5-12 million) per day. SAS and its pilots unions resumed talks on July 16 but failed to reach an agreement; they planned to meet again on July 18. If the strike winds up preventing SAS from accessing a debtor-in-possession loan, it might be forced to sell "valuable strategic assets under duress while also radically downsizing SAS’s operations and fleet." Anko van der Werff, President & CEO, said: "The strike is putting the success of the chapter 11 process and, ultimately, the survival of the Company at stake."

It's certainly not a given that SAS survives its court restructuring. Besides labor cooperation, the fate of SAS could ultimately hinge on the appetite for further government support. With Norwegian Air, Flyr and Norse Atlantic all flying, perhaps the region can do without a SAS? A separate question is whether SAS could attract interest from another airline. It clearly has some attractive assets, most importantly the Nordic corporate travelers tied to the carrier's EuroBonus loyalty program. - And SAS wasn't alone among European airlines in suffering labor unrest last week. Transavia, was also forced to cancel flights due to a strike by cabin crew. Separately, Transavia sibling KLM got some good news on July 14 in a new one-year accord with the unions representing its ground staff.

- Air France-KLM got some other good news last week. It finalized a €500 million ($503 million) perpetual bond from Apollo Global Management backed by a pool of Air France spare engines to repay part of the aid it received from the French government. The bond, which will be recorded as equity on Air France-KLM's balance sheet, carries a 6 percent interest rate for the first three years with step ups thereafter. The group can redeem the bond anytime after year three. The transaction is expected to close later in July.

- Returning to operations, Icelandair found an innovative solution to European staffing challenges. It is flying ground staff on passenger flights to Amsterdam to help turn the plane at the Dutch airport, and then having them return on the flight back to Reykjavík, reported Icelandic television broadcaster Ruv. No word on how long the airline will need to fly in staff to Schiphol.

- And in the U.S., United CEO Scott Kirby last week gave his take on the market's operational distress, appearing on the “In the Bubble” podcast. He pins much of the blame on inadequate air traffic controller staffing forcing delays and cancellations — much like Ed Bastian at Delta. “It’s like there’s a major thunderstorm across the United States every single day,” Kirby said. During the last four months, roughly 75 percent of United’s flight cancellations were due to FAA-mandated delay programs, he said, downplaying pilot availability. United is “overstaffed” with respect to pilots, having cut block hour capacity by about 14 percent from pre-pandemic levels, but pilot numbers by only 3-4 percent.

- But one airline's cancellations are another's financial boon. Wizz Air forecasts a “high-single digit” increase in RASM during the September quarter compared to 2019. This represents a nearly 20-point swing from the 10 percent year-over-three-years decrease in the June quarter. Load factors are on average more than 90 percent full this summer. “The fare environment remains strong, with industry capacity reducing and consumer demand over summer strong,” the Hungarian discounter said. However, Wizz is not entirely immune from Europe's operational distress. The airline cut its summer capacity forecast by 5 points to up 35 percent year-over-three-years.

- Aeromexico closed the buyback of its Club Premier loyalty program from Aimia on July 15. The $537 million deal for Aimia's 49.5 percent stake brings the program back in house to Aeromexico 12 years after it first sold the shareholdings. The deal was part of the carrier's U.S. Chapter 11 restructuring plan.

- New partnerships abound on both sides of the Atlantic. Air Canada and Emirates unveiled what they call a "strategic partnership," though details of the tie up suggest something more along the lines of a codeshare with some added reciprocal loyalty benefits. Call us old fashioned, but we think of a strategic partnership as something akin to an immunized joint venture or close to it. The new Air Canada-Emirates tie up begins later this year.

And in Europe, Norwegian and Widerøe signed an interline agreement that they plan to grow into something broader. Their new pact will eventually include "synergies relating to both other revenues and operational efficiencies" — what we would consider a strategic partnership. The partnership will connect Widerøe's regional network in Norway with Norwegian's European network, expanding travel options for travelers. - In Australia, regional turned mainline airline Rex has agreed to buy National Jet Express from scheduled charter carrier Cobham Aviation. The deal includes eight De Havilland Dash 8-400s and six Embraer E190s that National Jet operates under "Fly-In Fly-Out" contract services in Western Australia and Southern Australia. Rex sees its new Fly-In Fly-Out business as complementing its existing charter and airline operations around the country, and plans to expand it to Queensland and the Northern Territories. Terms of the deal that requires regulatory approval were not disclosed.