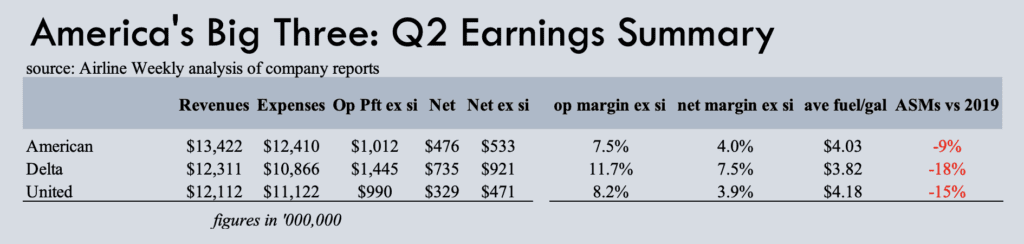

American Airlines was the earnings laggard before the pandemic. But will it be the laggard after? American, which entered 2020 with lower profit margins than Delta Air Lines and United Airlines, joined its rivals in returning to profitability in the second quarter. Encouragingly, its 7.5 percent operating margin was just fractions lower than what United posted. In fact, its 4 percent net margin was a bit higher than the Chicago-based carrier’s figure. On the other hand, both carriers lagged Delta’s 12 percent operating margin, and 7 percent net margin. Delta, however, had a key advantage last quarter: its oil refinery helped lower its average second quarter fuel price to an average of just $3.82 per gallon. American paid an average of $4.03 per gallon, and United (more exposed to the spike in east coast prices) $4.18.

American, to be sure, also had some important advantages this spring, which remain relevant this summer. Importantly, it has less exposure to the badly depressed Asian market, and more exposure to the well-performing Latin market, not least the booming beach markets in Mexico and the Caribbean. American is also the largest airline in Florida, another all-star market throughout the pandemic. Its Miami hub, for one, is much busier now than it ever was. Its Charlotte hub, keep in mind, is a top gateway to Florida. And American’s largest hub, Dallas-Fort Worth, has one of the country’s fastest-growing populations and economies.

Throughout the crisis, American has opted for a more aggressive capacity approach — its second quarter ASMs were down just 8 percent versus second quarter 2019, compared to United’s 15 percent drop and Delta’s 18 percent drop. That also has something to do with its smaller Asian footprint. Like United, American’s also constrained by Boeing delivery delays, failing to receive 787s it could have used to meet growing demand in markets like Europe. That said, it’s also constrained by Europe’s airport operations crisis, notably at London Heathrow where American and its partner British Airways have a leading position.

As for American’s own operational issues, CEO Robert Isom claimed that second quarter performance was better than it was in 2019. June, he admits, was a messy month, but mostly because 27 out of the month’s 30 days faced severe weather at its key hubs. “That weather resulted in ramp closures, ground stops, ground delay programs, [and] airspace flow programs, which had a ripple effect throughout our operations.” The only area of labor shortfall, Isom added, was for regional pilots.

Also in the call, American’s management spoke of its new alliances with Alaska Airlines and JetBlue Airways, which are boosting margins in two critical markets where it’s long underperformed, namely New York and Los Angeles. It discussed changes in business travel trends, including the impact of video conferencing, more flexible work arrangements, and less stringent enforcement of company travel policies. AAdvantage, its lucrative loyalty program, is seeing growth in enrollments. Latin markets remain “extremely strong.” International markets more generally are benefitting from the U.S. removal of Covid testing requirements in June, which will have a more significant impact on demand this fall (summer travel was mostly booked before June).

American, meanwhile, is negotiating a new mainline pilot contract, recognizing that labor costs — like most other costs — will further inflate. That makes it vital to reduce unit cost pressure by, in the words of Chief Financial Officer Derek Kerr, “getting the asset utilization where it needs to be.” That means first and foremost flying its planes more intensively, which won’t happen anytime soon as a scales back flying to ease operational stress. Also vital under these inflationary conditions: the resilience of current demand strength. On this, American appears confident based on advanced bookings into the fall.

United

United, as mentioned above, returned to the black with an 8 percent operating margin last quarter. As with other U.S. airlines, revenues are at all-time record levels. But so are much of the industry’s costs. Looking out for the next six to 18 months, United sees three major “storm clouds.” One is the operational distress impeding the industry’s ability to grow. Two is the high price of fuel. And three is the growing likelihood of an economic slowdown. On the latter point though, chief commercial officer Andrew Nocella said: “If a drop-off in cargo revenues is an early sign of a recession, we don’t see it.”

Like American, United talked about its London Heathrow frustrations (the airport recently capped capacity there). It also highlighted the difficulties of operating a hub at Newark Liberty airport, one of the country’s most congested. Exclude Newark, the airline said, and operating performance was largely in line with that of 2019. United also made the point that excluding Delta’s refinery benefit, its profit margins are among the industry’s best.

United’s heavy Pacific exposure, of course, is a drag currently, not least because it’s hampering its ability to fully utilize widebodies. Nevertheless, it has added or announced many new intercontinental routes, including San Francisco-Brisbane, Washington, D.C.-Cape Town, Tokyo-Saipan, and a slew of European and Middle Eastern markets (Amman, Bergen, Nice, Ponta Delgada, Palma de Mallorca, Tenerife, etc.). It has a new partnership with Virgin Australia as well, building on longtime alliances with carriers like Air Canada, All Nippon Airways, and Lufthansa.

The recent rejection of a tentative pilot contract notwithstanding, United plans to hire at least 200 pilots a month. For now, “the continuing pandemic recovery is more than offsetting economic headwinds.” And United is confident of reaching its goal of a roughly 9 percent pre-tax margin in 2023, rising to 14 percent by 2026.

Alaska

Alaska was one of the world’s most profitable airlines through much of the 2010s. After two years of crisis for all airlines, the Seattle carrier appears back to its old money-making ways. Its outstanding 14 percent operating margin last quarter came as demand recovered strongly, offsetting heavy cost inflation. Alaska did, importantly, pay less per gallon for fuel than even Delta — an average of just $3.76 per gallong thanks to hedging. It certainly helps right now to not have any overseas exposure, aside from some Asian demand connecting through its hubs. One secret to Alaska’s success during the past decade: its hometown Seattle, whose tech-heavy economy has grown far above the national average. The boom has been so spectacular that Alaska managed to withstand even a Seattle assault by Delta, which now operates a hub of its own there. Alaska, separately, is reaping big gains from its credit partnership with Bank of America, and its investment in more premium seats (though not ultra-premium transcontinental seats like JetBlue’s Mint product).

Alaska will before long retire its remaining Airbus A320s and A321neos inherited from its 2016 acquisition of Virgin America. De Havilland Dash 8-400 turboprops are exiting too, in favor of Embraer E-Jets. The staple of its fleet, however, will be the Boeing 737 Max. A partnership with American and year-old Oneworld membership adds more international options for its customers. Hawaii remains a critical market, one with lots of competitive capacity currently but also lots of high-yielding leisure premium demand. If anything, the biggest threat to Alaska, besides rising costs, is its exposure to a tech sector that’s now experiencing an uncharacteristic retrenchment. Seattle’s Amazon, for example, says it over expanded during the pandemic. Sure enough, Alaska said last week during its earnings call that corporate business volumes are “choppy.” And while “bookings remain at historically high yields,” those yields might have already “peaked.”

Mexican Twists

Aeromexico, out of U.S. Chapter 11 bankruptcy since March, managed a positive 3 percent operating margin for the second quarter, though its net result was a $47 million loss. Central to its operating profit was a recovery of demand, naturally, but also a 23 percent decline in non-fuel unit costs. That’s a testament to the power of cost cutting under the special rules of a bankruptcy court, where contracts become breakable.

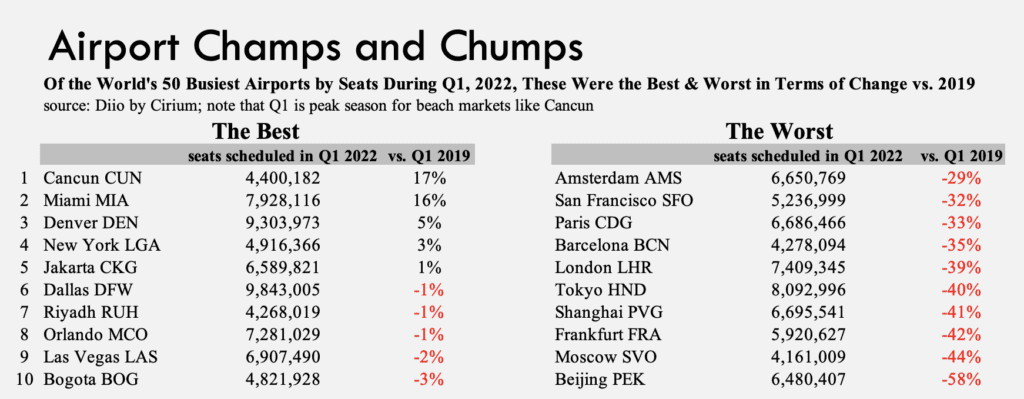

The Mexican airline market was a pandemic superstar of sorts, with beach markets like Cancun attracting a surge in visitors (see chart below). Cancun’s airport, indeed, is much busier today than it was before the Covid plague ever started — lax travel restrictions throughout the pandemic are a major reason. Unfortunately for Aeromexico, the Mexico City market was more typical in terms of traffic trends during the crisis. And its low-cost rivals Volaris and VivaAerobus were better positioned to take advantage of the beach boom. They also took advantage of Aeromexico’s downsizing while in bankruptcy, not to mention the collapse of Interjet, an airline that was barely able to survive before the pandemic (there’s talk, though, that it may return).

Aeromexico, with its new and improved cost structure, hopes to replicate the success of its low-cost rivals by leveraging close ties with Delta, the full acquisition of its loyalty plan, a new tour package division, and fresh capital provided by new shareholders led by U.S. investment fund Apollo. On the one hand, it faces frustrations with Boeing’s 737 and 787 problems, as well as with Mexico’s underperforming economy in terms of investment and output. According to the Financial Times, citing J.P. Morgan Chase, Mexico is the only major Latin American economy whose output will still be below pre-pandemic levels by the end of this year. Its overall economic growth over the past three years, meanwhile, has been among the weakest of Latin America’s larger economies. And on the other, there’s the frustration Aeromexico experienced several years ago, when its hopes to create a grand hub for the Americas fizzled with the cancellation — after construction had already started — of a brand new mega-airport for Mexico City.

Ever see a unicorn with a squirrel’s head? That’s probably less rare than an airline that did better in 2021 than it did in 2022. Well, sure enough, this was the case for Aeromexico’s low-cost rival Volaris. A year ago, it defied gravity with an extraordinary 23 percent second quarter operating margin, benefitting from a rush of newly-vacinated Americans flying to one of the few international places without travel restrictions, i.e., Mexican beach resorts. Fast forward to this year’s second quarter, and while Aeromexico reported a positive 3 percent operating margin, Volaris tumbled to a margin of negative 3 percent. The low-cost carrier said demand was “relatively strong,” though subdued by high inflation, economic uncertainty, and rising cases of Covid-19. Dramatically higher fuel costs, a weak Mexican peso, and lower bag revenues also proved painful, enough to create an improbable year-over-year collapse in margins.

Now, Volaris finds its U.S. expansion plans stymied by the Federal Aviation Administration’s downgrade of Mexico’s safety status. The carrier, owned by the same Indigo Partners that owns Frontier Airlines and Wizz Air, did say on a positive note that “we have not seen the operational issues that many international airlines in the U.S. and Europe are facing … The labor shortage issues regarding pilots and ground staff have not been a major factor here in Mexico nor in our U.S. operations.” It reports increasing difficulty in raising fares on some busy routes as well. On the other hand, bookings for the months ahead are strong, and Volaris hopes to win new business by expanding from alternative airports in the Mexico City area.

Finnair

Long-time readers of Airline Weekly will recall a recurrent theme in Finnair’s earnings. Year after year, the airline was, more or less, a one-trick pony relying heavily on routes to Asia. It was enough to stay decently profitably during the second half of the 2010s. But then came the pandemic, which led to a near-complete collapse of Asia’s international airline market, sending Finnair into a tailspin. To make matters worse, the Ukraine conflict left Russia’s vital airspace — not to mention the Russian market itself — closed to European airlines. In the meantime, China remains largely closed, and other key Asian markets like Japan have been slow to reopen. Such misfortunes showed in Finnair’s second quarter financial results, disclosed last week.

Finnair posted a $298 million net loss and a grisly negative 15 percent operating margin, usually the type of red ink it suffers during off-peak winters. Adding to its woes: Sky-high fuel prices, a weak euro that’s inflating its cost base, and Europe’s much-talked-about operational mayhem this summer. There are, mercifully, some bright spots. For one, Helsinki is one of the better-performing airports operationally this summer. Demand has almost normalized on short-haul routes within Europe, and is downright “robust” for its leisure tour operator segment. Demand is recovering well even on long-haul routes to the U.S. and South Asia, the latter including markets like India, Thailand, and Singapore. Cargo, too, remains strong (it was 16 percent of total second quarter revenues), though many busy cargo routes to Asia are longer now because of Russia’s airspace closure.

On the passenger side, Finnair flew 64 percent of the capacity it flew in 2019. That includes ASKs it is now wet-leasing to other airlines, including British Airways and Lufthansa, just to keep planes and crews busy while core markets recover. Finnair is trying new Helsinki routes to Dallas-Fort Worth and Seattle-Tacoma, alongside its new long-haul base in Stockholm, where it’s offering nonstops to Los Angeles and New York, as well as Miami this winter. Expansion from Stockholm is a direct attack on SAS, whose bankruptcy is both a blessing and a curse. Finnair will surely benefit from the Scandinavian airline’s two-week pilot strike. But assuming SAS makes it out of bankruptcy, it will surely do so with a more competitive cost structure.

Finnair is back to the drawing board on seeking more cost cuts of its own. It already extracted some savings from a new distribution deal with Amadeus. Roughly a year ago, it secured pilot concessions in areas like scope clauses, salary increases, and seniority. “There’s a track record of us being able to do structural renewal with our key employee groups like pilots,” the company said during its second quarter earnings call. That said, Finnair states clearly that it will lose money again in 2022, following losses in 2020 and 2021. Can it get back to the black in 2023?

In Other News

- Icelandair posted a small profit for the April-June quarter. It also said it expects to produce profits in the second half of the year, led by strength this summer. “Turning a profit in the second quarter is a major milestone on our road to financial sustainability,” CEO Bogi Nils Bogason said last week. In the second quarter, Icelandair operated 76 percent of its 2019 capacity. Management will have more to say about business conditions when it hosts a webcast with investors on Monday.

- SAS and its pilot unions reached a deal last week ending a 15-day strike. The airline said it secured key concessions and productivity improvements, while also committing to rehiring 450 furloughed crew members and honoring a 1 billion Swedish kroner ($97 million) unsecured bankruptcy claim. But the cost of the strike was high for SAS: not only did it lose $145 million and cancel some 3,700 flights, but the industrial action was the precipitating event that pushed it to a U.S. Chapter 11 bankruptcy filing on July 5.

- Air Canada and United are making a go of an immunized joint venture again, a decade after they dropped their last attempt after conditions they viewed as too onerous from Canadian regulators. This time, in what looks like a clear nod for regulatory approval, the airlines are “excluding certain U.S. leisure markets and territories” from their proposal. If successful, the duo of Air Canada and United in the U.S.-Canada market would be in a strong competitive position if, as rumor has it, Delta and WestJet also make another go at their own cross-border joint venture.

- Speaking of WestJet, the airline unveiled some of its first cuts from Toronto under a network restructuring that will see it return to focusing on its core Western Canada market. Flights between Pearson and Boston Logan end on October 29, and both Fredericton and Quebec City on November 14, per Cirium. In addition, budget subsidiary Swoop dropped its new Pearson-New York JFK route after just a month on July 18. The changes will WestJet exit Fredericton.

- The tumultuous operating conditions of the Covid-era produced yet another airline victim. Nigeria’s Aero Contractors, once considered one of West Africa’s most reliable airlines, suspended operations last week. But its maintenance and training divisions are unaffected. “The decision was carefully considered and taken,” the company said in a statement, “due to the fact that most of our aircrafts are currently undergoing maintenance.” It’s now “working assiduously to return to service as quickly as possible.”

- But just as old airlines disappear, new ones are born. In Canada, startup Jetlines announced the details of its inaugural flight, scheduled for August 15, between Toronto Pearson and Winnipeg. A few facts about Canada Jetlines: It’s focused on leisure flyers, using Airbus A320s deployed on routes to the U.S., Mexico, and the Caribbean. It will configure its planes in a high-density single-class layout.