Qantas Has a New CEO

There are few airlines that are held as high in the national consciousness as Qantas Airways is in Australia. That’s why the airline’s first new CEO in 15 years is such a big deal.

Alan Joyce, Qantas CEO since 2008, will pass the reins to group veteran Chief Financial Officer Vanessa Hudson in November. She will inherit an airline that is not only an iconic national brand but one that has emerged strong from the pandemic. During the first six months of the Qantas 2023 fiscal year, the airline posted an A$1.5 billion ($1.1 billion) operating profit and a 16 percent operating margin, besting its results in 2019. The airline expects a profit for the full fiscal year that ends in June.

Hudson will also, notably, be the airline’s first female CEO. And it will be the first time in Australian aviation history that the country’s two largest airlines, Qantas and Virgin Australia, are led by women. Jayne Hrdlicka leads Virgin Australia.

“This is an exceptional company full of incredibly talented people and it’s very well positioned for the future,” Hudson said in a statement. “My focus will be delivering for those we rely on and who rely on us – our customers, our employees, our shareholders, and the communities we serve.”

But credit for the strong Qantas that Hudson is set to inherit rests with Joyce. During his 15-year tenure at the helm of the airline, he fundamentally changed Qantas into a profitable aviation powerhouse — even if some contemporary travelers are grumpy with its customer service. He led the group’s domestic business from strength to strength, including forcing its main competitor Virgin Australia into administration in 2020. And Joyce is also credited with the success of Jetstar Airways, Qantas’ budget subsidiary, which he launched in 2003 and led until 2008. Jetstar continues to be a key lucrative piece of the Qantas Group.

Turning around Qantas’ longhaul international business was a cornerstone of Joyce’s legacy. When he took the helm of the airline during the Great Recession in 2008, longhaul flying was a money losing venture for Qantas. Its international business lost A$1.4 billion from fiscal year 2011 — when Qantas began breaking out results for its international business — through 2014. It turned a small A$267 million profit in the fiscal year ending June 2015.

Key to the international turnaround were new partnerships. After years of blaming, in part, increased international competition for the airline’s own poor longhaul results, Joyce changed tune and forged a partnership with Emirates in 2013. That pact allowed Qantas to restructure its operations to Europe, keeping just flights to London while shifting everything else to connections on Emirates via Dubai. Qantas has pursued similar partnerships with American Airlines in the U.S. — though that pact was not approved until 2019 — and Latam Airlines in South America in the years since.

Joyce’s turnaround of Qantas’ longhaul business set the stage for many of the initiatives that Hudson inherits. Top of the list is Project Sunrise, which will see the airline launch two of the world’s longest nonstop passenger flights between Sydney and both London Heathrow and New York JFK around 2025. Qantas has ordered 12 Airbus A350-1000s for the new ultra longhaul routes. The new nonstops will build on the existing flights to London from Perth that began in 2018, and the planned nonstop to New York from Auckland that begins in June. Hudson will take over Project Sunrise, which will test travelers’ appetite for very, very long flights.

Hudson will also need to manage Qantas’ international partnerships. Key is its joint venture with American, which has grown in importance during the pandemic as travel between the U.S. and Australia was one of the first transpacific markets to reach near recovery after Australia ended border restrictions in early 2022. In the second quarter, Qantas capacity between the U.S. and Australia is down 37 percent compared to 2019 levels — largely due to the late arrival of new Boeing 787s — while American capacity is up nearly 7 percent, according to Diio by Cirium schedules. Despite the lower capacity, Qantas has added one new U.S. route to its map since the pandemic: Melbourne to Dallas-Fort Worth, which is American’s largest hub.

More recently, Joyce is credited with Qantas’ successful navigation of the Covid-19 pandemic that all but shut down global air travel. The airline was lifted, in part, by its highly-profitable loyalty program that continues to generate 20 percent-plus profit margins for the group. But he has come under criticism from travelers over his handling of operational issues that plagued the airline last year, and a perceived worsening in customer service.

Restoring Qantas’ historic operational reliability and perceived customer service levels will be an immediate challenge for Hudson. Joyce, during the carrier’s most recent earnings call in February, highlighted aircraft delivery delays at both Airbus and Boeing, and staffing and training issues as two of Qantas’ most pressing issues. The former is not expected to ease until at least the end of this year, which raises questions about the delivery timeline of the airlines’ narrowbody refleeting with new Airbus A220s and A321neos that are due to begin arriving during the fiscal year ending in June 2024. Staffing issues are also expected to abate in the 2024 fiscal year.

Hudson, as a finance executive, is seen as well prepared to manage Qantas’ fleet renewal. Aircraft capital expenditures through fiscal 2026 are estimated at $5 billion, and investors and analysts will be watching closely how the airline pays for the planes while maintaining investment-grade credit metrics.

Lufthansa Bullish on Summer

Things are looking up in Frankfurt. The Lufthansa Group, Europe's largest network carrier, sees all the elements falling into place for a significant improvement in operating profits this year.

Travel demand remains robust. Cost pressures are easing despite significant investments in operational aspects of the business to avoid a repeat of last summer's rampant flight delays and cancellations. And the group sees a permanent shift to more premium leisure travel that supports its big investment in new first, business, and premium economy cabins dubbed Allegris.

“The Lufthansa Group is on track," CEO Carsten Spohr said during a first-quarter earnings call last week. The group posted an adjusted €273 million ($302 million) operating loss, and €467 million net loss, in the first quarter; not an unusual result for the weakest three months of its year. Its operating margin was negative 3.9 percent.

Lufthansa, however, sees money to be minted this summer. Spohr said the group is "on the verge of the strongest summer in our company's history in terms of traffic revenue." Yields, a proxy for airfares, are forecast up roughly 25 percent over 2019 levels in the second quarter; for comparison, yields were up only 10 percent from 2019 levels during the June quarter last year. The only area of demand weakness is in corporate travel, which at the end of the first quarter was down 40 percent on volume and 30 percent on revenue from four years earlier.

The group anticipates an adjusted operating profit of more than €754 million — its result in 2019 — during the second quarter. Its full-year adjusted operating result outlook is more than €1.5 billion is unchanged, though analyst consensus has risen to roughly €2.2 billion for the year — an estimate that Chief Financial Officer Remco Steenbergen declined to affirm or reject.

But Lufthansa's forecasted summer revenues are not solely the result of torrid demand. The airline industry's capacity constraints, including labor and, increasingly, aircraft availability, mean carriers will fly less — in some cases a lot less — than they want. More travelers and not so much more capacity means airfares, and yields, will rise.

"I've been around 30 years in this industry, [and] I've never seen anything like it — basically spare parts are missing," Spohr said. He referred specifically to the issues plaguing Pratt & Whitney geared turbofan engines on Airbus A220 and A320neo family aircraft. The Lufthansa Group currently has three A320neo family planes, and a third of Swiss International Air Lines' 30 A220s parked due to the shortage in spare parts for their P&W engines, Spohr added.

In India, Go Air filed for bankruptcy last week citing losses that stemmed from the delay of P&W-equipped A320neo family aircraft. In the U.S., Hawaiian Airlines has five of its 18 A321neos on the ground awaiting parts, and Spirit Airlines has had to cut its capacity outlook for the rest of the year due to grounded A320neos awaiting parts. And in Europe, AirBaltic has resorted to wet-leasing aircraft to make up for the number of A220 aircraft it has parked awaiting parts.

There is a "global shortage of spare engines," Air Lease Corp. CEO John Pleuger said Monday. Efforts to address this by P&W and other engine suppliers, he added, has diverted production capacity from engines for new aircraft, further delaying deliveries from both Airbus and Boeing.

Lufthansa executives did not comment on how many of its own new aircraft deliveries could be delayed this year. However, Spohr did say the airline plans to debut its new Allegris premium cabins on the 787 in the fourth quarter.

The Lufthansa Group maintains its 2023 capacity forecast of 85-90 percent of 2019 levels. Second quarter capacity will be roughly 82 percent of levels four years ago, or an 8.5 percentage point improvement from a year ago.

One benefit for Lufthansa this summer is the return of its Airbus A380s in June. The decision last year to return the 509-seat superjumbos to service was made with the view that the airline needed the capacity lift to meet travel demand amid aircraft delivery delays, particularly of Boeing's new 777-9. Lufthansa will reintroduce the A380 on flights from Munich to Boston on June 1, and to New York JFK on July 4, according to Diio by Cirium schedules.

Lufthansa continues to negotiate with the Italian government on its planned purchase of ITA Airways, Spohr said. If finalized, Rome would be a strategically important southern European hub for flights to Africa and Latin America for the group that now counts Zurich as its furthest base south. And the airports in both Milan and Rome have excess capacity that gives the Lufthansa Group needed opportunities to grow. One thing that Spohr was clear about is that the group does not intend to turn ITA into a dominant force in the Italian domestic market, which is now dominated by budget airlines and train services.

"The Italian government clearly considers the Lufthansa Group as the best home that will ensure a good future for its national airline. Our talks here are on the right track," he said. The deadline for a deal was recently pushed back to May 12.

In the first quarter, the group's passenger airlines posted a combined €512 million adjusted operating loss, or half the loss a year ago. Only Swiss was in the black with a €77 million adjusted operating profit. Lufthansa Cargo and Technik also reported profits during the period. Unit revenues (RASK) were up 25 percent compared to 2019, and unit costs (CASK) excluding fuel and currency were down slightly year-over-year but up nearly 18 percent from four years earlier.

Iberia Leads IAG's Winter Profits

When it comes to Europe’s Big Three Airlines, it’s not even close: International Airlines Group — the owner of British Airways, Iberia, Aer Lingus, Vueling, and Level — is consistently the most profitable. This was true again in the first quarter of 2023, with the Lufthansa Group and Air France-KLM both reporting red ink at the operating level (margins of negative 4 percent and negative 5 percent, respectively). IAG on the other hand, eked out a small first quarter operating profit, a commendable achievement for the slowest period of the year.

Iberia led the way with a positive 5 percent operating margin, up from negative 2 percent in 2019. It saw “strong leisure demand in all regions.” The Madrid-based airline is also seeing a faster pace of recovery in business travel than at other airlines. Iberia’s specialty is Latin America, where it competes most directly with Air Europa, an airline IAG will acquire if regulators allow. IAG chief Luis Gallego said during Friday’s earnings call that the regulatory review process should take about 18 months. In the meantime, Iberia is also strengthening its U.S. network in part by adding capacity through increases in aircraft utilization.

British Airways earned a first quarter operating profit as well, albeit just barely (its 2019 operating margin was much better, at positive 8 percent). The carrier was always more dependent on corporate travel, which IAG fears will never come back to quite where it was in 2019. “We don’t think that corporate travel will get back to 100 percent,” Chief Financial Officer Nicholas Cadbury said. He gave a level of around 80 percent as the most likely scenario, and “probably at the lower end of that range for this year in British Airways.”

But leisure demand is strong at British Airways, and just as Iberia’s core South Atlantic franchise is performing well, so is British Airways’ core North Atlantic franchise. This franchise, don’t forget, benefits from a close revenue-sharing joint venture with American Airlines. By all industry accounts, North Atlantic markets will produce exceedingly strong profits this summer, which should translate to strong second and third quarter profitability for British Airways.

That’s also the case for Aer Lingus, even more dependent on North Atlantic markets. Its first quarter operating margin was an unsightly negative 23 percent, substantially worse than the negative 9 percent it reported for the same quarter of 2019. But it’s well positioned to recover these early-year losses thanks to robust leisure demand originating in the U.S. Shorthaul leisure routes are booking well too. Aer Lingus is feeling a pinch, however, from a sizable exposure to tech sector travel, which is currently weak.

Finally, with respect to Barcelona-based Vueling, its first quarter operating margin improved from negative 17 percent in 2019 to negative 12 percent in 2023. Vueling’s business is also highly seasonal, yet it reduced first-qiarter losses thanks to well-performing winter sunshine markets like the Canary Islands and Egypt. The LCC is also enjoying solid gains in ancillary revenues and mitigating offpeak losses is a high priority (having a more consistent flight schedule across seasons can also help with operational performance). Vueling, however, given Barcelona’s proximity to France, has been “significantly disrupted” by a wave of French air traffic controller strikes. These have also caused headaches for British Airways, which is simultaneously dealing with constrained capacity at London Heathrow.

One important driver of IAG’s first-quarter operating profit was cheaper fuel. The company said the average spot price of jet fuel during the quarter was $910 per metric ton, down approximately 5 percent from the same quarter a year ago. Prices dropped as the quarter progressed, peaking at $1,140 per metric ton in late January but falling sharply to $805 per metric ton at the end of March. IAG has roughly 60 percent of its expected fuel needs hedged at about $810 per metric ton. Another contributor to the company’s first-quarter strength, importantly, was its Avios loyalty program.

IAG is cautious about what might become of the economy, what might happen with fuel prices, and what operating conditions might be this summer, given further threats of strikes and airport staffing shortages. But for now, it’s raising its full-year profit guidance based on what it sees from forward bookings. “We see strong demand everywhere.”

ANA, JAL Beats Forecasts

All Nippon Airways and Japan Airlines beat profit expectations during the fiscal year ending in March as international travel demand rebounded. Inbound international travel demand increased “dramatically” in the fourth quarter, ANA said. This helped propel its full year operating profit 120 billion Japanese yen ($875 million), and operating margin to 7 percent. In February, ANA forecast a roughly 90 billion Japanese yen operating profit and margin of around 5.6 percent. The airline reported a net profit of 90 billion Japanese yen for the year ending in March.

JAL saw similarly strong demand for international travel but focused on high yields for connecting services between North America and Asia via Tokyo's Narita airport. It expects this trend to continue citing the easing of travel restrictions to China. JAL posted a 64.5 billion Japanese yen operating profit, or a 34.4 billion yen net profit, and a 4.7 percent margin. That beat its forecast of a 50 billion yen operating and 25 billion yen net result from February. However, JAL's results did not beat its original 80 billion yen operating and 50 billion yen net forecast from earlier in the fiscal year.

The turnaround is good news for Japan's big two airlines. Unlike competitor Korean Air, which posted profits on the back of strong cargo demand throughout the pandemic, travel restrictions and a smaller cargo business kept ANA and JAL in the red for two years. However, beginning in October, Japan ended its final Covid entry restrictions and lifted caps on inbound tourist numbers. That allowed travel to the country to surge, even during the historically lower demand winter season.

The number of visitors entering Japan has picked up dramatically since October. Nearly 1.48 million foreign visitors entered the country in February, according to the latest data available from Japan National Tourism Organization. That is equal to 57 percent of 2019 levels, and a dramatic 48 point rebound since September.

ANA recovered to nearly 68 percent of its pre-pandemic international capacity in the March quarter. Traffic recovered to 65 percent of 2019 levels, and all-important yields were 45 percent above four years earlier.

JAL, on the other hand, flew 94 percent of its pre-pandemic capacity (measured in ASKs) in the March quarter. Passenger traffic was 88 percent recovered. International yields were up 37 percent, while domestic yields were roughly flat.

Looking ahead, ANA expects strong inbound visitor demand to Japan in its 2023 fiscal year that ends next March. Outbound travel demand is forecast to “recover gradually;” something that has hit carriers dependent on Japanese travelers, Hawaiian Airlines for example, particularly hard. ANA expects international passenger numbers to rise to roughly 80 percent of 2019 levels by the March quarter of 2024, and domestic passenger numbers to plateau at around 95 percent.

ANA forecasts a net profit of roughly 80 billion Japanese yen in the 2023 fiscal year. It anticipates a 140 billion yen operating result and a 7.1 percent operating margin. One challenge for ANA this year, as for nearly every other airline, is rising costs. Expenses are forecasted to rise at least 15 percent year-over-year.

JAL forecasts continued strong international and connecting demand driving a 55 billion yen net profit during the 2023 fiscal year that ends next March. It anticipates a 100 billion yen operating profit.

First-Quarter Earnings Round Up

- It's now beyond dispute: Chinese tourism is back, at least domestically. The South China Morning Post reported that 247 million people traveled by air, rail, waterway, or road within or out of mainland China during the Golden Week holiday at the start of May. That number, the Post points out, is equivalent to the entire combined populations of Japan, Australia, the UK, and the American cities of Los Angeles, Houston, Chicago, and Phoenix. With travel spending up less than travel volumes, questions remain about the vigor of China's post-Covid economic rebound, and what it means for global economic growth. For airlines though, recovery is clearly underway, evident even during the first quarter. Air China and China Eastern again reported steep quarterly losses, plagued by heavy exposure to intercontinental markets which are still depressed. The two carriers posted negative 14 percent and negative 16 percent first quarter operating margins, respectively. The more domestic-oriented China Southern, however, held its margin deficit to just negative 5 percent. For Hainan Airlines, it was just negative 1 percent. And the LCCs Spring and Juneyao were already back in the black last quarter, with margins of positive 10 percent and positive 6 percent, respectively. It certainly didn't hurt that fuel prices fell throughout the quarter. With domestic travel now roaring back this quarter, expect much more black ink from Chinese airlines in the next reporting season.

- During the dark days of the pandemic, Korean Air's lights shined bright. The carrier was in fact more profitable than ever during the crisis, and in some quarters more profitable than any other passenger-focused airline worldwide. The secret to its success was its large cargo business, which boomed during the pandemic. That's now cooled, but Korean Air continues to deliver strong if not quite so spectacular profits. Its first quarter operating margin was 13 percent. Cargo accounted for a third of total revenues in the quarter, compared to 77 percent during the same period last year. The cargo business is now dealing with "low demand." But passenger demand has recovered strongly, boosted by the reopening of China and Japan. Passenger load factor in the first quarter rose to 82 percent. Longhaul demand is strong. Leisure demand is strong. Shorthaul demand is improving. Sixth-freedom transit demand through Seoul is strong, notably linking the Americas and Southeast Asia (think Vietnamese and Filipino Americans flying to visit family). One final travel restriction not yet lifted in the first quarter was China's ban on overseas group tours. Korean Air is undertaking some major strategic moves, most importantly its planned takeover of rival Asiana, pending regulatory consent (specifically from the U.S., the EU, and Japan). It's also adding lie-flat seats to some of its narrowbody planes and developing its joint venture with Delta.

- Speaking of Delta joint ventures, before the pandemic few imagined that Latam, South America's largest airline, would ever go bankrupt. It was known as one of the industry's profit leaders for many years. Lo and behold, with its passenger business devastated by Covid and government assistance largely unavailable, Latam joined other Latin American carriers like Aeromexico and Avianca in U.S. bankrupt courts. Bankruptcy restructurings are never easy, but in Latam's case, the proceedings helped it achieve an impressively low non-fuel cost structure, one even lower than what it had in 2019, never mind all the general inflation that's ensued since. This helped it achieve an almost 11 percent first quarter operating margin, up from just 3 percent in the same quarter of 2019. Latam is a big cargo player, and cargo demand has weakened. But passenger demand is strong, notably on longhaul routes including those to the U.S. and Europe. The one major exception is routes involving Peru, due to social unrest. In Brazil, Latam's largest market, the carrier is benefitting from a benign competitive situation, with Azul and Gol its only main rivals. Those two airlines, incidentally, did not go through bankruptcy and are thus still plagued by heavy debts. Latam for its part currently has no significant non-fleet debt maturities in the next 4 years. Post-bankruptcy, the Cueto family behind Latam owns just 5 percent of the airline (down from 16 percent). Delta and Qatar Airways each own 10 percent (down from 20 and 10 percent, respectively). The carrier's largest shareholder, which used to be Delta, is now the investment firm Sixth Street, with 28 percent. Delta is a key strategic partner too; the two airlines have a new joint venture emanating from Latam's pre-pandemic decision to ditch its old partner American. The new JV will soon launch two new routes, namely Sao Paulo-Los Angeles and Bogota-Orlando. Brazil, Chile, Colombia, and Peru are Latam's Big Four markets, having closed its Argentine venture several years ago. One analyst wondered whether it might look to Mexico next, perhaps teaming with Delta's close ally Aeromexico.

- The first-quarter earnings season is now finished in the U.S. Allegiant and Frontier both reported last week, finding themselves in very different situations. The former (based in Denver) posted a negative 3 percent operating margin, while the latter (based in Las Vegas) registered at positive 15 percent. Frontier for its part spoke of strong demand, thanks to people having more flexibility than ever to travel. Ancillary sales, a big part of its business model, were strong too. But non-fuel cost inflation is a problem. Frontier is now sacrificing some unit cost efficiency by adopting a new network strategy that complies with what it sees are altered travel patterns. More specifically, peaks are getting peakier and offpeak days even quieter. "By maximizing flying on peak days and peak periods and reducing underperforming flying in low demand periods, we believe we can generate better profitability with less flying, thus derisking our operations." This will result in cutting some longhaul routes, which are operationally harder to schedule only on peak days. But even as this puts upward pressure on unit costs, Frontier expects to retain a major cost advantage versus peers. And more importantly, it expects to return to double-digit profit margins later this year.

- As for Allegiant, its network always peaks in the first quarter, so no surprise to see it perform so well. Interestingly, it stressed the excellent level of profitability for its credit card product. Allegiant's number one priority: new pilot and flight attendant contracts. Note that Allegiant like other carriers has felt compelled to trim capacity in an effort to preserve operational reliability. "This is a result of MRO delays for aircraft and heavy maintenance [and] pilot constraints, along with airport construction disruption and ATC delays in some key markets, particularly during peak travel days." In other Allegiant matters, its new Sunseeker hotel will open this fall. The airline will go live with its new Navitaire reservation system this quarter. As of now, its first Boeing 737 Maxes will arrive at the end of this year. And it should soon (pending DOT approval and an upgrade to Mexico's aviation safety rating) be able to start a joint venture with VivaAerobus.

- Speaking of VivaAerobus, it lost money in the first quarter, just like its rival Volaris. Operating margin was negative 6 percent, better at least than the negative 15 percent it suffered in 2019. The LCC should perform well for the full year, now that the weak offpeak season is past. Mexico finds itself with a major opportunity to grow its economy, capturing manufacturing work currently done in China. Some however raise cautionary flags, citing infrastructure shortcomings, hostile federal government policies, and drug war violence.

- Cebu Pacific of the Philippines produced its first profitable quarter since the pandemic started. From January through March, Cebu's operating margin was positive 6 percent. The airline said both passenger demand and ancillary demand was strong. "[Cebu] expects that in the second quarter, it will exceed its pre-pandemic capacity on a systemwide basis, supported by an optimistic outlook as the tourism industry continues to recover, plus the strengthening of its Clark and Cebu hubs."

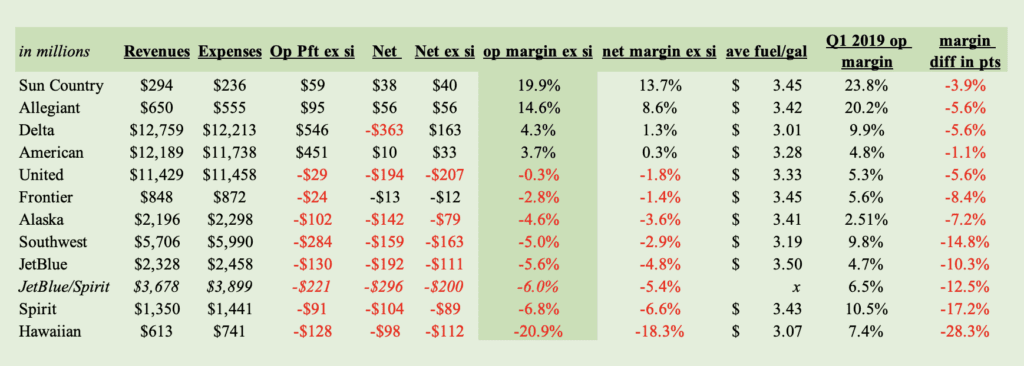

U.S. Airlines First-Quarter Earnings Scorecard