Singapore Airlines is Thriving

Singapore Airlines, one of the world’s most esteemed airline brands, wasn’t all that esteemed in financial circles last decade. Not that it ever lost money. But the commonplace double-digit operating margins of its past ended in 2010. During the next four years, margins wallowed between 1 percent and 3 percent. Things steadily if modestly improved after the oil crash of 2015, and operating margin reached a post-2010 high of 7 percent in 2019. Then came the pandemic losses — mitigated some by cargo strength — but also generous government aid and thorough cost restructuring.

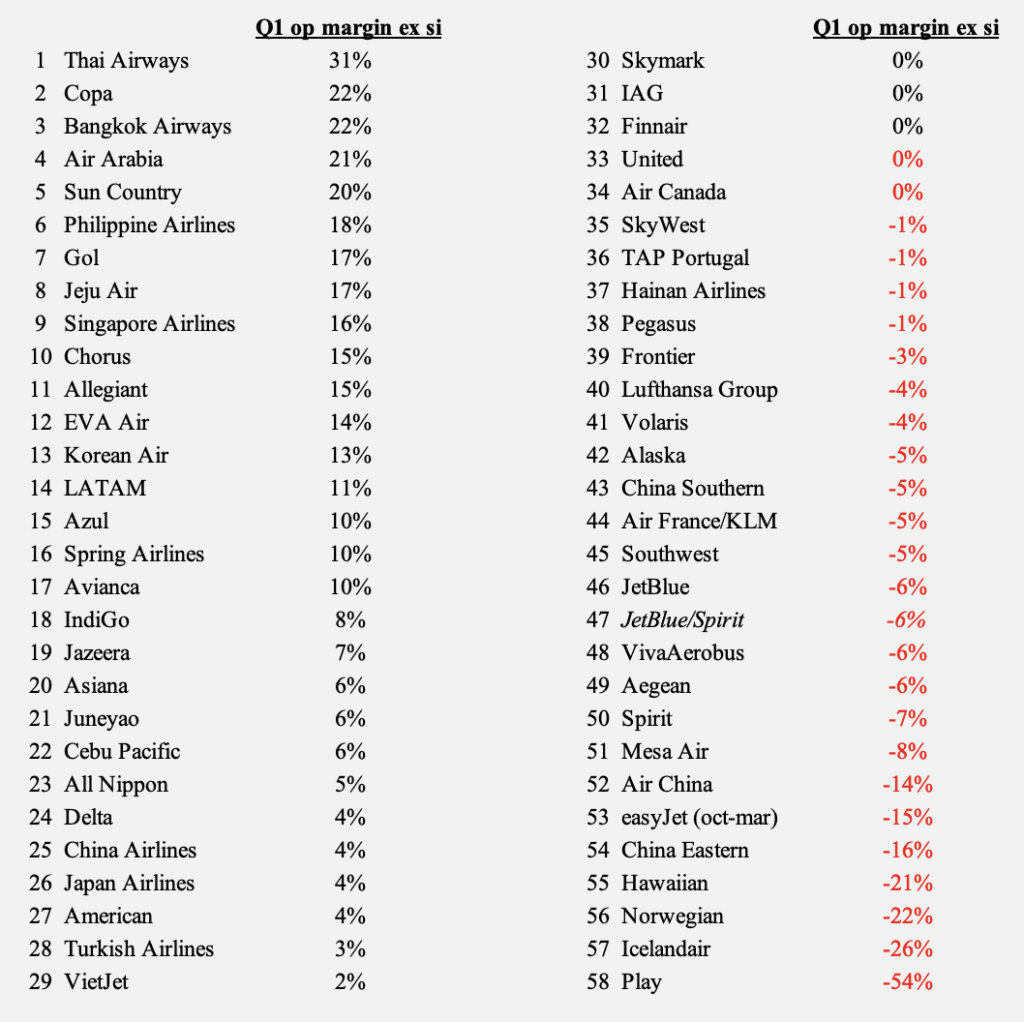

When passenger demand began reviving in mid-2022, Singapore Airlines was once again earning impressive profits — some of its highest profit margins ever, in fact. In the just-completed first quarter of 2023, the airline’s operating margin was 16 percent, consistent with a common theme across much of East Asia: Airline profits are soaring, outside of China and Japan anyway, where the comeback has thus far proved more muted. Singapore Airlines deserves credit for re-hiring and recruiting new crews even before Covid travel restrictions were lifted, ensuring it was ready to take advantage of the demand revival as soon as it started. The company continues to report strong passenger demand across all cabins going into the northern summer season, though cargo demand has become “not great.”

Strategically, the airline is placing a big bet on India by purchasing a 25 percent stake in the new Air India, which will incorporate Singapore’s current Indian airline Vistara. It’s “extremely excited” about the reopening of the China market, which will strengthen as the holiday tour operator market ramps up. It’s surely disappointed by Boeing’s 777-9 delays but will lengthen leases on 777-300ERs to compensate. It also downplayed the impact of engine issues at its low-cost subsidiary Scoot, which flies Pratt & Whitney-powered Airbus A320neo-family aircraft. Scoot, by the way, will soon start flying Embraer E190-E2s. Collectively, Singapore Airlines and Scoot are still flying less capacity now than they were in 2019. But they’re hoping to pursue longterm growth as Singapore’s Changi airport opens both a fifth terminal and third runway in the years ahead.

India's IndiGo Targets 100 Million Passengers

Not yet 20 years old, India’s IndiGo has grown to become a colossus in its giant home market, assuming a role not unlike Southwest in the U.S. According to Diio by Cirium data for the current April-to-June quarter, IndiGo now flies more seats and operates more flights than even Turkish Airlines or EasyJet. But this might just be a preview of bigger things to come. Clearly, IndiGo has the itch to go longhaul, if not quite yet ready to commit. It’s already dipping its toe in the waters by operating leased Boeing 777s from Turkish, itself partnering with IndiGo to gain more access to India’s fast-growing market. IndiGo is also codesharing with other carriers, including American, Qantas, Virgin Atlantic, Qatar Airways, and Air France-KLM — IndiGo’s CEO Pieter Elbers held the top job at KLM for many years. Regarding its international ambitions, Elbers said in the LCC’s calendar first-quarter earnings call: “As time will progress, we’ll evaluate some of these possible new opportunities.” The airline has long been attacking international markets within narrowbody range, and international markets happen to be outperforming their domestic counterparts at the moment, broadly speaking. They tend to have lower unit costs after all, because stage lengths are longer on average.

Overall, IndiGo produced a solid 8 percent operating margin last quarter, which follows an outstanding October-to-December quarter. It’s now dabbling in cargo freighters and intends to improve its loyalty plan. As longer-range Airbus A320neo-family aircraft arrive, new low-risk international opportunities beckon. IndiGo’s A320neos and their engines, to be sure, have created Taj Mahal-sized headaches for IndiGo. But an airline that’s gained so much scale and clout has the flexibility to source acceptably-priced substitute capacity when needed.

IndiGo is nothing if not a survivor, outliving a parade of hapless rivals from Kingfisher to Jet Airways to most recently GoFirst. It naturally has close eyes on Air India as it attempts to become a reputable competitor with support from Singapore Airlines. Newcomer Akasa Air too appears hungry to grow. But IndiGo is certainly not intimidated. It’s targeting to move no fewer than 100 million passengers this fiscal year (wow!) and trumpets itself as India’s leading airline. “Our philosophy here is, wherever you have to go in India, you have to go IndiGo. That’s precisely our philosophy, India by Indigo.”

More First-Quarter Earnings...

- In mid-April, EasyJet disclosed its financial results for the six months between October and March, its offpeak winter half. Recall that operating margin for the period was negative 15 percent. Last week the carrier held a call with investors to provide more detail about the half, and about what lies ahead. Critically, the airline has finally put an end to massive operating losses in Berlin — more than $100 million in 2018 and another $100 million-plus in 2019. Doing so involved major capacity cuts in Germany. But other areas of the network are growing, notably busy beach markets like Portugal, Greece, and Egypt. EasyJet is expanding from the UK as well, in part with more domestic flying in the wake of Flybe’s demise. More importantly, though, management says outbound leisure demand from the UK remains strong despite the country’s economic misfortunes, with Brits now prioritizing their summer holidays, even ahead of home renovations and dining out at restaurants. Along with the strong demand environment, EasyJet sees revenue growth potential from its profitable Holidays division (a tour operator), its ever-improving ancillary prowess, and its more reliable operations. Cheaper fuel and a weaker U.S. dollar certainly don’t hurt. But what about the competitive threat from the ultra-LCCs Ryanair and Wizz Air? Not to worry, executives assured: “Ryanair is adding 10.5 million seats this summer, Wizz was adding 5.8 million seats this summer. Of the Ryanair capacity, 1.1 million is head-to-head with us. Of the Wizz capacity, actually, it’s a reduction of 400,000 seats with us. So net, if you combine the two, it's 700,000 extra seats on our 56 million seats for this summer. That's 1.25 percent. So actually, they are growing, but they’re not growing on our network.”

- In Europe, Greece’s Aegean Airlines limited its first-quarter operating losses, ending with a margin of negative 6 percent. That’s perfectly acceptable for what’s a super-seasonal airline. The Greek economy, mired in a deep depression a decade ago, is benefitting from strong tourism, even in the absence of Russian arrivals. And so is Aegean, an airline that’s held its own against low-cost carriers like Ryanair and Wizz Air. This summer, Aegean is offering 16 new destinations, including several in the Middle East. Notice, by the way, how European carriers are becoming more and more active in the Middle East, aided by longer-range narrowbodies.

- Like its rival Gol — which likewise managed to avoid bankruptcy despite a lack of pandemic-era government support — Azul is currently producing impressively high operating margins but also worryingly high net losses. The Brazilian carrier, launched by JetBlue founder David Neeleman 15 years ago, simultaneously managed a positive 10 percent operating margin and a negative 16 percent net margin. The red ink stems from heavy interest payments on debt that accumulated during the pandemic and swelled further because of a weak Brazilian real. Just last quarter, Azul incurred $230 million in interest payments. Mercifully, air travel demand in the Brazilian market is currently strong, with yields elevated by limited competition — just three main airlines now prowl the Brazilian skies (Azul, Gol, and Latam). Azul is also enjoying newly-won slots at Sao Paulo’s downtown Congonhas airport, plus a wellspring of profits from auxiliary businesses, specifically a tour operator, a loyalty plan, and a cargo/logistics business. One fun fact mentioned in the carrier’s first-quarter earnings call: Azul’s tour operator has become the largest seller of Disneyworld tickets in Latin America. The company is now launching a maintenance, repair, and overhaul (MRO) shop, “Azul TechOps,” which will insource work from other airlines. It’s great timing, given the worldwide shortage of MRO capacity. At the airline itself, fleet renewal is a major theme, with more A320neos and Embraer E2s on the way in, and first-generation Embraer jets on the way out. What investors are most concerned about, however, is its debt, which Azul reassuringly says will drop sharply thanks to new agreements with Airbus, Embraer, and lessors. The next big step is securing agreements from bondholders. “I would just like to remind everyone,” said the Azul’s CEO John Rodgerson, “that we’re returning our leverage to 3x in 2024 without any government support, without using bankruptcy or other judicial restructuring processes, and without imposing a haircut on our creditors as other airlines around the world did.”

- How long will Asiana remain an independent airline? Its pending takeover by Korean Air remains subject to foreign scrutiny, and the EU for one said last week it has some reservations. For now, the independent Asiana is enjoying the post-pandemic Asian upswing, earning a 6 percent operating margin in the first quarter. That, however, is less than half the 13 percent Korean Air managed in the same quarter. Believe it or not, Asiana reported a 15 percent operating margin during last year’s first quarter, when passenger markets were still largely closed — the cargo boom explains why. Cargo is now much weaker, but passenger demand is back with a vengeance. Separately, the independent Korean LCC Jeju Air reported as well last week. Its operating margin was an impressive 17 percent. That suggests Korea’s domestic and shorthaul international markets (specifically, Japan, greater China, and Southeast Asia) are currently thriving.

- Skymark, a Japanese LCC, eked out a positive 0.2 percent operating margin for the year’s first quarter. It’s an airline with a checkered history, at one point recklessly ordering A380s. Before long it was bankrupt but saved from oblivion with financial help from Airbus (All Nippon stepped in as a shareholder as well). It’s now back on the Tokyo stock exchange, hoping to compete in the Japanese domestic market. This time it’s being responsible and taking Boeing 737 Maxes, including eventually -10s — no more widebody pretensions. One current tailwind is the preference of many would-be Japanese international tourists to travel within Japan instead, a trend Skymark attributed to the weak yen and high inflation abroad. Japan’s government, furthermore, is subsidizing domestic tourism to help revive the sector. The airline also hopes to win more slots at key airports including Tokyo Haneda, Kobe (near Osaka), and Fukuoka. For its full fiscal year that just began in April, Skymark is forecasting a 6 percent operating margin.

- A few other first-quarter earnings updates from around East Asia: VietJet, a fast-growing LCC, returned to the black with a 2 percent operating margin. More interestingly, Philippine Airlines continues its remarkable turnaround, echoing that of its regional rival Thai Airways. Both were bankruptcy-plagued loss-makers before the pandemic but extraordinarily strong profit producers now. PAL’s March quarter operating margin was — wait for it — 18 percent. In Taiwan meanwhile, Eva Air greatly outperformed China Airlines, 14 percent versus 4 percent. Eva’s significantly greater North American exposure was presumably helpful. Both Taiwanese carriers, by the way, are dealing with a well-funded new rival — Starlux — intent on grabbing a piece of Taiwan’s longhaul market; Starlux is now offering nonstops to Los Angeles.

- TAAG, the national airline of Angola, cut its losses from roughly $300 million in 2021 to more like $60 million in 2022. The carrier has ambitious plans to grow its fleet from 20 to 50 aircraft in the next four years, supported by new partnerships with carriers like Iberia and Gol. Angola is an oil-rich nation with linguistic and thus economic links to Portugal and Brazil. Note that IATA will hold a Focus Africa conference in Addis Ababa next month, addressing the market's opportunities for airlines. As IATA said: “Over the next 15 years, Africa’s passenger traffic is expected to double. The continent stands out as the region with the greatest potential and opportunity for aviation. But this potential is limited by infrastructure constraints, high costs, lack of connectivity, regulatory impediments, slow adoption of global standards, and skills shortages, among other factors."

First-Quarter Earnings Scoreboard

- Keep seasonality in mind as you look at these figures. Note for example that the first quarter is peak season in Thailand (not to mention Florida where Sun Country prowls) but offpeak in most major markets.

- Ranked by operating margin excluding special items.

Bank of America Transportation Conference Highlights

- Alaska Airlines: “At least through this summer, we’re going to have really strong demand.” So said Alaska’s Chief Financial Officer Shane Tackett, echoing a common sentiment across the airline industry. Most businesses (especially smaller businesses) are traveling in full force, and leisure travel is so good this year that Alaska regrets not flying more capacity last quarter to popular vacation spots. Some of Alaska’s best markets right now include Latin and Central America, the state of Alaska, and Florida (which it serves trans-continentally from West Coast gateways). Hawaii demand is strong, though competitive capacity is elevated (Southwest is now a major player). Business conference travel to places like Las Vegas and San Francisco is coming back. Most importantly, outbound demand from the airline’s Pacific Northwest strongholds is strong — from Seattle for sure and even from Portland, Ore., despite post-pandemic economic woes for the city’s downtown core. There are, however, some exceptions to the rosy demand story. Alaska still sees weakness among West Coast tech giants, whose travel remains “still pretty depressed,” down some 40 to 50 percent from 2019. In a related trend, Bay Area transcontinental flying has been among the least recovered segments for the airline. Tackett separately spoke about the demand help Alaska is receiving from its American and Oneworld partnerships. He denied any major disruption concerns regarding Boeing and its Max deliveries. And regarding possible structural shifts in demand patterns, like people flying more on certain days of the week than before, he’s “not ready to declare any new normal.”

- Frontier Airlines by contrast is convinced that unit revenues have become much stronger on peak days and much weaker on offpeak days. “What we’ve seen is in the off-peak periods, the difference between peak day RASM [revenue per available seat mile] and off-peak day RASM has grown. It’s grown from peak days having a 19 percent unit revenue premium … to a 26 percent premium," Vice President of Commercial Daniel Shurz said. In response, Frontier is adopting more accordion-like schedules, flexing capacity up and down depending on the day of week. That’s harder to do operationally on longer-haul transcontinental routes, so it’s dropping some of those. Schedules are also becoming optimized for operational reliability, which has indeed improved in recent months. Frontier insists that its ultra-low-cost carrier model still works, dismissing a growing chorus of skeptics who say supply-side shortages will create barriers to one of the model's essential ingredients: rapid growth. Shurz highlighted, among other things, the carrier’s large Airbus orderbook and growing ancillary revenues — it’s on track to reach an average of $85 in ancillary revenue per passenger. He asserts that Frontier is still the lowest cost producer in the industry, never mind the upward unit cost pressure from operating fewer longhaul flights and prioritizing reliability. Yes, demand is healthy, so much so that it’s the first time Shurz can remember, in his 20-plus-year career, that as fuel prices increased, “we were able in the industry to get revenue to go up enough to more than cover [the added expense]. He specifically mentioned strength in shorthaul international demand, which includes a lot of family visit traffic. He also cited Puerto Rico as a market that’s currently thriving. Dispelling the notion that ultra-LCCs are flying Walmarts, catering to America’s poor, Shurz said more than half of Frontier’s customers have household incomes above $100,000. (Median household income in the U.S. is about $70,000).

- Sun Country’s Chief Financial Officer Dave Davis said average income across all his customers is “a little south of $100,000 a year.” He said peak versus offpeak RASM differentials by day of week are about 25 percent. Like Allegiant, Sun Country practices an extreme form of accordion scheduling, with offpeak capacity roughly half what it is during peak periods. Davis separately said pilot attrition rates have dropped sharply since signing a new pay contract. Demand to Florida, he added, is almost insatiable. And in east coast markets like New York and Boston, he suspects that “legacy fares have gotten so high that small businessmen are trading down to us and flying on us.”

- Air Canada’s outgoing Chief Financial Officer Amos Kazazz expressed the challenges of cost inflation, as well as the difficulties of demand forecasting. A new distribution strategy should help some on the cost side. On the demand side, strength is visible across all geographies through the summer, and even into the fall. Booking curves, he said, are normalizing. But one thing Air Canada will be watching closely is whether premium demand stays strong if the economy weakens. Kazazz downplayed the threat of Canada’s crop of young low-cost carriers, insisting Air Canada has the tools to effectively defend itself.